There was no safety net. We didn't sell anything. There was no inheritance from a long lost uncle. We didn't live on beans and rice or move in with anyone.

Most families don’t have these options available and must find other ways to attain financial freedom. My husband and I haven’t sold anything, we both work full-time, we homeschool our kids, and don’t have the time to pick up a side hustle.

We budget hard, track every dollar, cut expenses, and make sacrifices whenever we can.

This is a particularly special post for us, because we are celebrating a major milestone on our payoff journey. More importantly, I want all of you to know that we aren’t just writing about this stuff, we are actually doing it. These are real strategies and budgeting tips for real people, just like us!

You can reach your goal without having to sacrifice the things you love!

Let me be really real with you guys. For most of my marriage, actually my life, I’ve been a spender. From the time I started earning my own money, I spent every dollar as soon as it hit my account, never saving or even thinking about the future.

As soon as I turned 18, I got two credit cards, immediately maxed them out, and got stuck in a cycle of making those minimum payments while drowning in interest rates. I added student loans and was in over my head before I even turned 20. Instead of paying down the balances, I went out and bought a new car, adding even more debt to my tab. There was no plan!

I got married at 21, and my husband was a budgeting, saving, frugal guy. His eyes almost came out of his head when he saw my finances, or lack thereof, but he didn’t give up on me. He helped me get it under control, pay off all of the credit cards and learn how to live within my means. He got us on a budget, which I followed (loosely) to what I thought was the best of my ability. I still wasn’t very good at it, and I strayed more and more over the years, often regressing to my old overspending habits.

It was a huge adjustment, because retail was my favorite therapy. When our circumstances changed and my husband told me our new debt payoff plan, I was more than hesitant. I can still remember him telling me we were drastically reducing all spending and tightening the budget, and the only thing running through my mind was how badly I wanted to keep the new pair of Lululemons I had quietly ordered the day before. (Good news – I got to keep them!)

I heard the words coming out of his mouth assuring me we could do this super tight budget and it sounded great, but deep down I didn’t know if I had it in me. That all changed when we sat down and created a real plan with goals. We both committed to each other and our financial future. Something clicked in me, and I knew this was my time to prove I could do this for myself and our family. See how it all started in The Frugal Payoff – A debt free journey.

Fast forward 8 months —

Month 8 - January 2021:

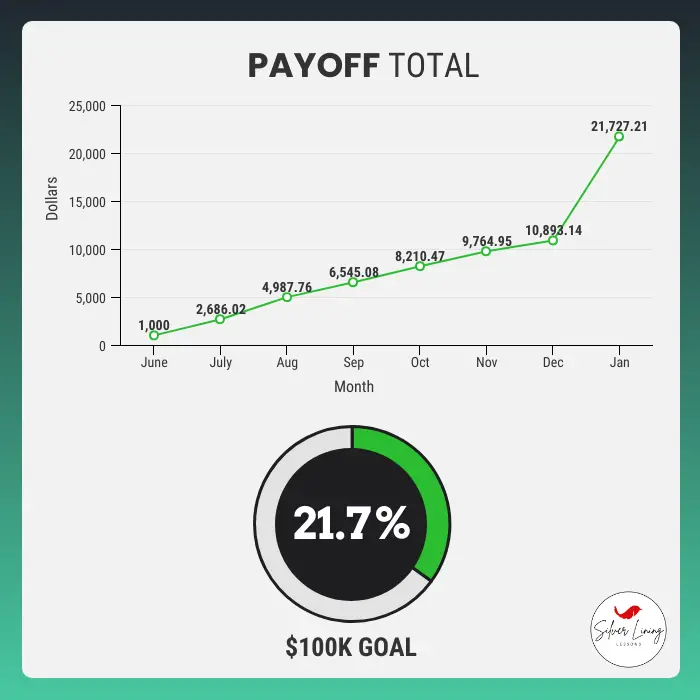

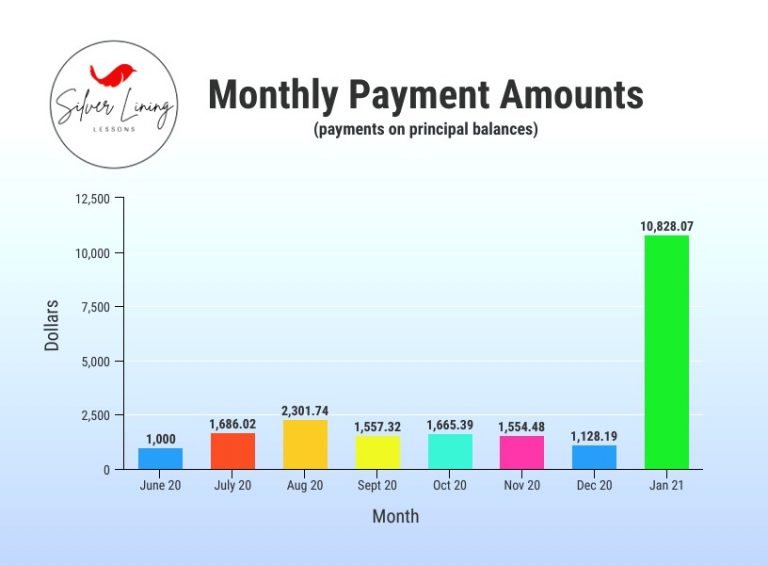

$10,828.07 of debt paid down

We knew going in that this would be our biggest payoff month to date. We switched over to the the Free Cash Flow Method towards the end of the last year and liked the security of making it through the holidays with cash on hand above our emergency fund. While continuing to pay down debt to meet our monthly target of $1,666, we were able to tuck away my husband’s bonuses from November and my bonus from December. Believe me, it was so difficult not to spend any of this extra money on our kids for Christmas or buy each other gifts. This is where doing all our holiday shopping in October really delivered.

Utilizing the Free Cash Flow Method, we calculated two large bills we wanted to pay off in full on top of our monthly target, and we made it happen. Those bigger payments are a little harder when it comes down to it. Seeing thousands come out of your account at once is tough, but seeing that balance owed hit ZERO is beyond rewarding.

Debt Paid: $10,828.07

Total Progress: $21,721.21

Like I said, this wasn’t a normal month. If you are curious about our previous monthly updates, you can find those posts here:

Show Me The Money: $7k in First Four Months

Money Talks: Yearend Payoff Update [$11k and On The Way]

Where do I start when paying off debt?

Establishing an emergency fund and having a budget meeting is a great place to start! This is how we kicked off our big payoff plan with The Baby Emergency Fund and The Budget Meeting – $1,000 Monthly Savings.

When paying off debt, what should I pay first?

You first have to see how deep your financial hole is, face your number, and pick your strategy. It’s going to be painful and sometimes the truth hurts. Kinda like ripping off a band-aid, it will only hurt for a second. Once its over, the immediate pain subsides and you can begin to let the scars of your financial past heal. In Debt: Finding your number, then finding your way out , we talk about pulling your head out of the sand, ripping off the band-aid, and finding a way out.

There have been ups and downs. We haven’t picked up second jobs, side hustled or increased our income, mainly because of the pandemic and homeschooling. We also haven’t sold anything. We’ve done all of this by strict budgeting, cutting back expenses, and learning what is important to us – things we wished we had known before.

You can read all the books and blogs, listen to the podcasts and talk to the experts, but you have to put in the hard work to hit your goals!

These are lessons I have learned and keys to success in reaching our first major milestone.

- The Dollar Tracker: Y’all, this is the number one thing that opened my eyes to just how much overspending was killing my budget. If you haven’t done this yet, you really should give it a try. Head over to Why The Dollar Tracker Makes More Cents for more on this literal gamechanger!

- Not Eating Out: This sacrifice is hard. Early on, I dreamed of Taco Bell and Chick-Fil-A, but the cravings were gone once I saw the dramatic savings! Check out Six Months Without Eating Out – Woah! to see how I broke up with eating out and even made our own menus at home.

- Cutting Expenses: We completely redid our budget and cut everything we possibly could, immediately eliminating $1,000/month! One of our biggest savings was the cable bill. See How I Saved $1,800/year Cutting Cable.

- Get Creative: You don’t have to go cold turkey and give up everything you love! You don’t have to eat beans and rice like Dave Ramsey yells. Get creative and substitute when you can. I’ve learned that I can still have the little luxuries I enjoy but just on a budget. For example, I switched from my fancy vitamin subscription service to ordering my own in bulk (Back to the Basics: Vitamins), saving over $450/year. We did research and traded in the expensive energy drinks and Starbucks (R.I.P. iced lattes) for cheaper alternatives (More Bang for Your Buck: Energy Drinks). After more research (Loaded Teas: Are They Worth It?), we replaced the trendy loaded teas with our own recipe – The Frugal Loaded Tea (Loaded Tea Recipes – DIY).

THE STRUGGLE IS REAL WHEN PAYING OFF DEBT

While everything I’ve said so far sounds fine and dandy, it hasn’t exactly been a bed of roses. When you first start paying off any amount of debt, big or small, it feels great. You may be able to breeze through your smallest debts, and with each one you eliminate, you feel that rush. Immediate progress!

The truth is it becomes more challenging as you get into the larger debts. It may feel like you are getting nowhere, even though you are still making progress. You’re tired of saving, stretching a dollar, working long hours, and making sacrifices.

This is debt burnout, and you have to push through it – remember your WHY!

Debt burnout is completely normal and expected. It’s that feeling of being tired/annoyed with your day-to-day routine or the lack of flexibility in your budget. You’re frustrated and ready to give up. At this point, you are deep in the “I want steak, but all I get is this chicken” mentality. Years of living a caviar life on a tuna fish budget made it especially difficult for me to push through when all I wanted to do was jump ship and splurge on expensive takeout.

BUT REMEMBER – Debt is an easy hole to fall into and an easy hole to climb out of as long as you stay focused and stay motivated. Becoming debt free will not happen overnight!

- Listen to other people’s debt free stories -I’m not really a big Dave Ramsey guy. I tend to think he is a little loud and obnoxious, but I absolutely love the debt free shout outs at the beginning of his podcast. There are tons of other stories online to hear success stories from people in various situations with different amounts of debt. Hearing the joy and relief in their voices helps me imagine hitting my goals.

- Take a break and find frugal ways to have fun – Use your newfound frugal learning to develop low cost hobbies. Our family has bonded over puzzles and board games, which we then swap with friends and family. For more ideas, jump over to 10 Highly Effective Habits of Frugal People.

- Celebrate the wins -Pick a target and reward yourself when you hit it! For my husband, he wanted (really needed) a new laptop but committed to buying it only when we hit the $20k milestone. Instead of replacing his 10-year-old MacBook with another expensive Apple, he downgraded to a more budget-friendly option. For me, it was ordering a few new shirts for work (Jane.com for the win) and a new book.

- Talk about your struggles with others – I use this blog as an outlet. Find your outlet or dive into personal finance books. The more you talk and learn, the more normal your struggles will feel. It’s easier to hold yourself accountable and stay on track when you are talking to others about paying off debt. The key is surrounding yourself with supportive and positive people to encourage you along the way. I would love to hear from you and help if I can, even if it’s just to offer support and cheer you on!

- Stay motivated with money challenges – Target the areas where you are trying to save the most money or pay down debt, and incorporate monthly and/or year long challenges into your plan. We are set to start our first monthly budget challenge next month. If you are looking for a challenge, check out our Financial Fitness in 2021 to see which amount fits your budget.

Remember to SUBSCRIBE and FOLLOW US to stay up to date on all things Silver Lining Lessons!

**The links in this post are affiliate links. This means if you click on the link and purchase an item, I will receive an affiliate commission at no extra cost to you. All opinions remain my own.

© 2024 Silver Lining Lessons